Maxwell Marlow has narrated this article for you to listen to.

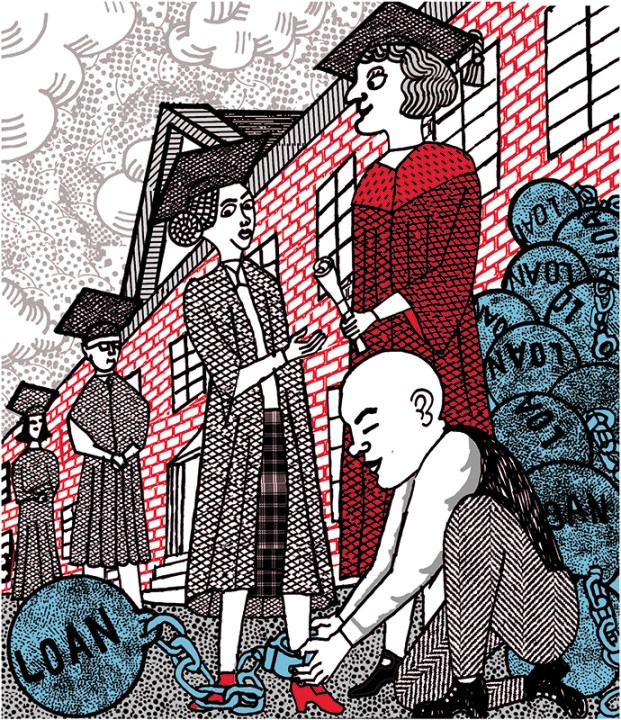

England’s student debt is staggering. It comes to £270 billion – that’s larger than the budget for the NHS and two and a half times larger than the education budget. This arsenal of taxpayer-backed cash has seen the creation of 34 new universities just to feed an ever-hungrier mass of undergraduates. It’s forecast that by the late 2040s, this loan balance will reach £500 billion.

These loans are not standard financial arrangements. They don’t affect the debtors’ credit ratings, only their mental health when they check their bank balance. Crucially, most loans are also wiped after 30 years from graduation. In order to offset the generous cost of clearing the loans of the nearly half of students who won’t be able to repay them, the interest rates increase as the graduate earns more.

Universities hold no liability for whether they provide an education that leads to a successful career

In her most recent Budget, the Chancellor decided to freeze the repayment thresholds for student loan deductions for Plan 2 students. Plan 2, being the most numerous of the student loan plans, has an interest rate of 3.2 per cent for those unlucky souls earning more than £28,470, rising to 6.2 per cent for those earning over £51,245. This has caused an outcry from the usual quarters who think that all education should be ‘free’. The New Statesman’s Oli Dugmore has argued that the changes to thresholds are regressive, while self-styled ‘money saving expert’ Martin Lewis has urged Rachel Reeves to ‘do the right thing’ and U-turn.

Those of us who believe in free-market economics are in a more difficult position. Right-wing economic orthodoxy can be boiled down to: ‘If you use it, you pay for it.’ Education is no different. In theory, then, fiscal right-wingers should be in favour of student loans. However, the state’s involvement in the process has caused a mélange of poorly thought out, left-wing practices that, yes, the Conservative party was largely responsible for. There are price controls, for instance, capping the fees so that engineers pay as much as humanities students, despite the different capital requirements for teaching and expected earnings afterwards. Here lies the great hazard to the public in the time-dependent loan wiping, making taxpayers liable for debtors unable to pay off the loan. And universities hold no liability whatsoever for whether they provide an education that leads to a successful career or produces an unproductive and unprepared graduate.

The situation is particularly precarious for many younger graduates. According to the Higher Education Statistics Agency, the ‘£24,000 to £26,999 salary band contains the highest proportion of graduates aged 24 years and younger’. For context, the annual pre-tax pay of a worker on national minimum wage is £25,396. Many graduates move to cities in the hope of a decent career but find that their rents are high and the cost of living is expensive. They then struggle to afford their student loan payments on a salary no higher than if they hadn’t bothered with university at all. Many of them may conclude that their degree simply wasn’t worth it.

There are exceptions, such as engineers, finance graduates with jobs in the City and medics after ten years in our health service. But for the rest of the graduate class, it’s bleak. Owing to usurious interest rates and a graduate market plagued with poor capital investment, higher input costs and economic growth in the dregs, it feels like most young graduates have been dealt a 7-2 offsuit, in poker terms.

We must change the higher education sector to better meet the needs of both the volatile and fast-paced global economy and Britain’s exposed fiscal state. The Adam Smith Institute, where I work, has calculated that public debt will climb to 330 per cent of GDP by 2075. The evolution of the student loan book will make this even worse if we do not change our growth and borrowing strategies. A heavily indebted and grumpy workforce, trained in the wrong skills and paying through the nose for that training, will only make it harder to avoid bankruptcy.

What can be done about the student loan situation in a sustainable way? In 2020, Donald Trump announced a student loan pause. This cost US taxpayers $195 billion. A British equivalent would obviously be unaffordable, so there must be other options.

The government would be wise to abolish the wipe-away clause in loan contracts which lets taxpayers take the hit from millions of unpaid loans. If debtors fail to repay the balance, they should be subject to repayments during retirement and inheritance, given the already generous nature of the taxpayer to recover these costs. This would then allow the government to reduce the exorbitant loan interest rates.

If the government wishes to make education free, then that is their prerogative, but they cannot afford to do so without significant tax rises and reliance on international credit. There is only one answer that solves the current conundrum. Hard choices, honesty and squaring with the debtors. Anything else ends in ruin. Sadly, given how governments love to woo taxpayers with unaffordable promises, we’re probably heading for the cliff edge.

Comments