I am standing in the village Co-op with my eight-year-old daughter when she asks, inevitably, to be bought a magazine. As most parents will know, magazine is a generous term for this iteration: a collection of sorry pages whose sole purpose is a vehicle for plastic toys. I say no, but then she blindsides me. ‘Fine, I’ll pay for it with my pocket money,’ she declares, whipping out her pre-paid card like a good capitalist. As I slip the packet of fags I have bought for myself into my pocket, I realise that I am morally snookered. For is she not free to spend her pocket money as she likes? And am I not free to spend my money as I like? Libertarians, all.

Most of us born before the advent of digital banking will have firm ideas about pocket money. It was the 50p coin handed over on a Saturday morning for good behaviour, the penny slotted satisfactorily into the chipped piggy bank, the shiny gold coin proffered by a great-uncle with bristling nose hair at Christmas. Both talisman and symbol, pocket money represented the transition from innocence to maturity, or the bridge from the murky world of feeling into the cold rationale of capitalism.

The idea of pocket money was popularised in Your Child Today and Tomorrow (1912)by American parenting guru Sidonie Matsner Gruenberg, who railed against the meanie puritanical impulses of early 20th-century parents, declaring that ‘children should have toys’.

Had Gruenberg stood in the doll aisle at Home Bargains on a cold Saturday morning, she may have changed her mind. Prior to formal theories on pocket money, gold coins were veritably tossed all over Victorian and Edwardian children’s literature, with avuncular figures doling them out, largely it seems, to make children ‘run along’.

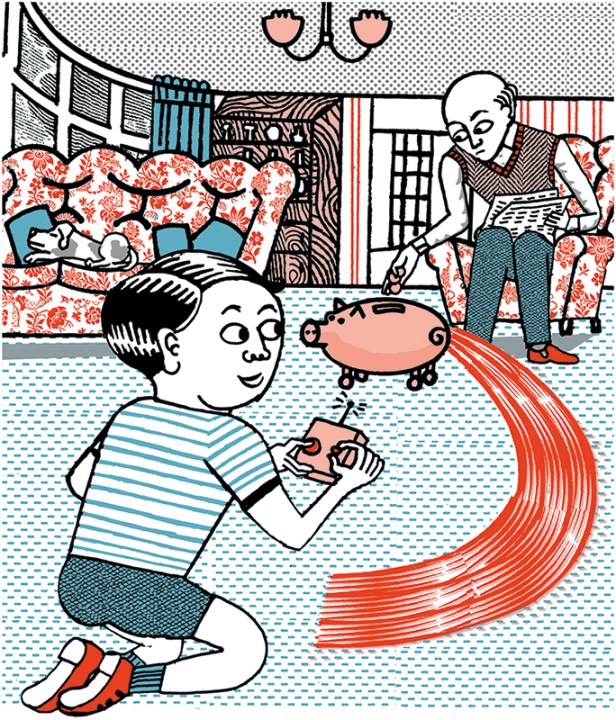

But in our modern, cashless society the coin is long gone. The penny given to spend in the sweet shop has been replaced by an app on your phone in which you can transfer money to your child at the touch of a button, all neatly displayed in bright infographics to show them their ‘financial journey’ from the age of three upwards. For today’s children, there are no secrets or even privacy: Big Mother is watching. Yes, they may feel as if they have autonomy via their natty pre-paid debit card, but the app means that we ‘helicopter parents’ can see exactly what the shiny gold coin is being spent on. Capybaras, mainly, in case you were wondering, although this seems relatively innocent when you consider that, according to the NatWest pocket money index for 2025, gaming was the number one expenditure.

In search of answers – or simply meaning – I speak to Will Carmichael, CEO of Rooster money, the pocket money app bought by NatWest in 2021. Mr Rooster is suave and old-school. In a former age I suspect he would have been a merchant banker; in the Fintech era he is still winning, except he wears a baseball cap and not a pocket watch. Gamely, he greets my scepticism and piggy bank nostalgia head on. Pocket money is no longer given arbitrarily, he says, but is rather ‘a paradigm’ or ‘a meaningful way of engaging with money from an early age’. I listen carefully as he talks me through the ‘inflection points’ of acquiring a debit card (typically at the age of eight) and tries to convince me of ‘meaningful’ ways that children can ‘think about value exchange’. I already know what children think of value exchange – they have a more guerrilla approach – but I don’t say this. Cynically, I think of all the little Rooster customers who will stay with NatWest for life. Certainly, pocket money apps are spreading across the high street banks at a rate of knots – Starling bank and Monzo, to name but two, accompanied by other stand-alone apps such as GoHenry, which levies a monthly payment of up to £9.99 from parents.

But I can see that Carmichael has a point. I believe my own staggering financial illiteracy is the result of never having been given pocket money, but rather being dealt random handouts (with a novelist for a mother, we had no ‘cash flow’ as the not-broke millionaire Woody Allen memorably put it).

By 2028 all children will have mandatory lessons on budgeting, saving and even fraud protection

But financial literacy isn’t just a buzzword for fintech tycoons, it’s spreading to the national curriculum. By 2028 all children of primary school age will have mandatory lessons on budgeting, saving and even, somewhat alarmingly, fraud protection. Throw away the abacus, because the children of the future will be far more financially literate than their debt-ridden parents. Given the astonishing rates of student debt in this country, this can only be a good thing. Perhaps the recently appointed Treasury select committee for the tax burden faced by graduates may wish to use a colourful app with teddy bears to incentivise repayments.

Another Saturday and we’re back in the Co-op. As per our individual financial freedoms, I am buying fags and a copy of Private Eye with my pocket money. ‘Would you like anything, darling?’ I ask, whipping the offending items away. ‘No, thank you,’ comes the little voice, ‘I’m saving up for an Apple watch.’ Given the rates of compound interest on her £1.50 a week, I calculate that this purchase may be some way off. In any case, I’ll be able to block it via the app.

Comments